Jacob Wackerhausen/iStock via Getty Images

Performance

During the second quarter of 2026, Night Watch Investment Management LP appreciated by 12.80% net of fees.

Last quarter, we mentioned that our shareholding in Marex (MRX) had grown to be an outsized position in our portfolio, at 14.5%. This paid off this quarter, with the stock up 37% in the quarter and 230% since we bought our first shares around the IPO two years ago. The company is benefitting from high market volatility, while simultaneously showing great execution on their M&A playbook, most notably by continuing to grow their prime brokerage business. At 10x 2026 P/E and >30% ROE, this remains a compelling long.

Performance this quarter was further aided by strong performance of names such as Watches of Switzerland Group (WOSG LN) and Silicon Motion (SIMO). We owned two noticeable detractors: FUTU (FUTU) and Sanuwave (SNWV). We have been adding aggressively to FUTU while we are waiting for improving data points before risking more capital on SNWV.

Portfolio

Night Watch manages a global value strategy that differentiates on the following points:

Catalyst – We predominantly buy value companies with an identifiable catalyst for a rerating. Catalysts can include industry tailwinds or company-specific events (e.g., earnings inflection, CEO changes, refinancing).

Inside Ownership – We aim to find companies where management has considerable ownership in the company. We consider this alignment of interest to be an important determinant of share price performance.

Unique Names – To differentiate from a long list of other value strategies, we seek unique portfolio holdings that have little overlap with a typical wealth management portfolio. We aim to provide our LPs with diversification from their other investments in addition to strong performance.

The portfolio as of June 30th, 2026, is as follows:

Largest positions:

- Marex (13.7%)

- AAR Corp (7.3%)

- Remitly (6.2%)

- Distribution Solutions Group (5.8%)

- Universal Technical Institute (5.8%)

- Adyen (5.6%)

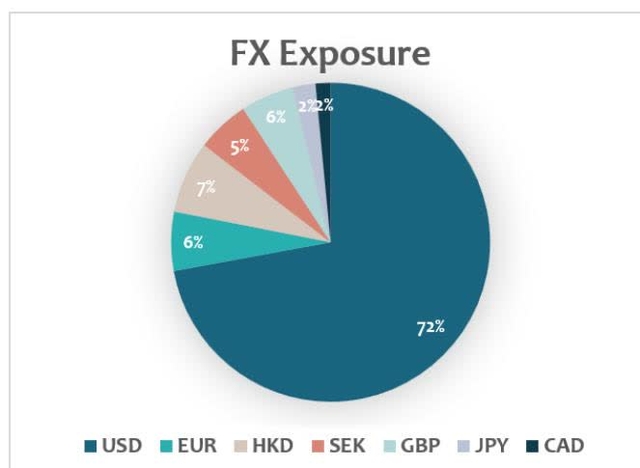

FX Exposure

Pie chart showing FX Exposure by currency: USD (72%), EUR (6%), HKD (7%), SEK (5%), GBP (6%), JPY (2%), CAD (2%).

Market Update

The first half of the year has been unusually volatile, and the market has been even more bifurcated than usual. On the one hand, you have got businesses that touch AI, whose stocks keep going up daily to what we believe to be unsustainable levels. We are not complaining. We were early on Western Digital Corp (WDC) and we still own Silicon Motion (SIMO). Both benefitted from the shortage in memory caused by strong demand from AI data centers. But we are not blind to the cyclical nature of those businesses, and we have been early in taking some chips off the table.

On the other hand, you have got everything that is not AI. If your business is a quality compounder with a decade-long history of providing your shareholders with 10-15% earnings growth, your stock got sold off because why would anyone care about 15% per year if you can earn that in a day by holding AI stocks!?

Naturally, we are buyers of such businesses. If we can find low-risk ways to lock in 15% earnings growth, and if we might even get some multiple expansion on top when markets normalize, we are happy to move up on the quality spectrum. We added quality names including Stryker (SYK), Adyen (ADYEN NA)(ADYYF) and Booking.com (BKNG).

Finally, there were the companies that, rightly or wrongly, were viewed as AI losers. We were reminded once again that valuation in today’s market does not provide a floor to stock prices. Especially software and payment related companies saw their shares freefall during the first half of 2026.

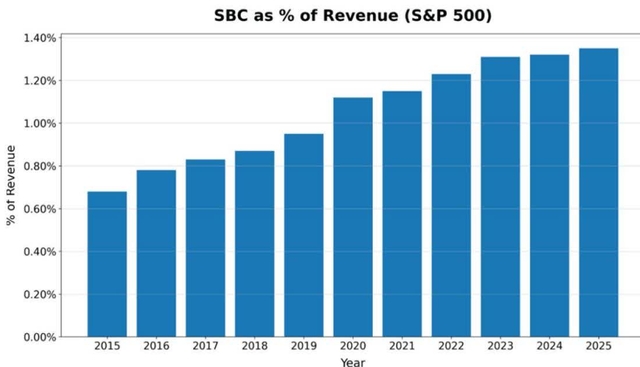

We have a differentiated view on this sell-off. Over the last few years, we have seen an increasing reliance of companies on Stock-Based Compensation (SBC). Growing a business requires capital. Wall Street’s greatest trick was to convince the markets that this growth could be funded without running the costs through the P&L. If you simply paid employees through stock options or stock grants, they argued, it’s not a real expense, and analysts ought to exclude it from their model.

For some reason, Wall Street obliged. SBC took on excessive levels as companies were keen to exploit this newly found loophole.

Source: KEDM.com – Companies taking Wall Street for a ride by excluding from earnings all salaries paid out in options and stock grants.

It isn’t hard to see the reflexive nature of this setup. Paying in SBC and excluding those costs is all fun and games when share prices go up. But when share prices go down, the dilution caused by the SBC goes up. 3% dilution per year can quickly become 10% dilution. On top of that, your employees are seeing the value of their stock options dwindle and might be quick to start thinking about updating their resumes.

Now that the market has finally started caring about SBC, it seems wise to buy companies with real earnings.

Historically, Dutch companies have paid out little to no SBC. This is not by accident. Stock options or grants in The Netherlands are taxed excessively, making this not a viable option for companies. While that’s a shame for Dutch employees, it benefits shareholders of those companies.

Companies with international operations, who have a large portion of their employees in places like Amsterdam, have a comparative advantage. BKNG and ADYEN fit that bill. For the first time since inception, Night Watch is going Dutch. We added BKNG and ADYEN to the portfolio.

Position Highlights

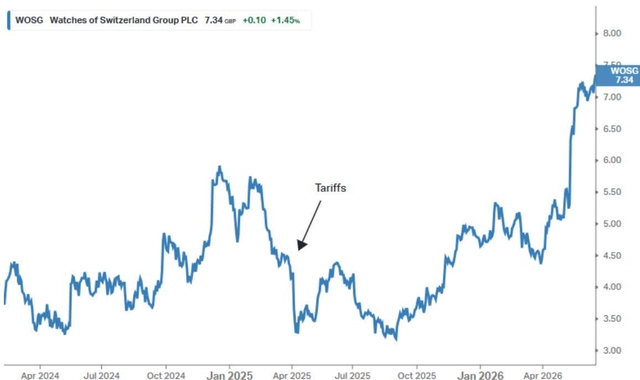

Watches of Switzerland Group (WOSG LN)(WOSGF) has been a core position since our inception in 2024. It has been a somewhat frustrating investment for the first two years, but more recently the stars have started to align.

WOSG is a retailer of luxury watches, most notably an authorized dealer of Rolex and Patek Philippe. This business is considerably higher quality than ordinary retailing because it is supply-constrained rather than demand-constrained. Prospective buyers often have to join waiting lists for popular models, and the number of watches a retailer sells is determined largely by the allocation it receives from Rolex rather than by end-market demand. Rolex, in turn, is owned by the Hans Wilsdorf Foundation, a non-profit organization that appears to be at least as interested in preserving its Swiss legacy as it is in maximizing profits.

The business model over the last few decades has been straightforward. Rolex consolidated the sale of its watches among a small group of trusted partners with the financial strength to invest millions in dedicated Rolex stores and the ability to provide a consistent customer experience across locations.

WOSG was the consolidator in the UK. In exchange for accepting slightly lower gross margins, it received larger allocations from Rolex. Higher volumes per store more than offset the lower margins.

Following its success in the UK, WOSG replicated the model in the United States, which today accounts for roughly 50% of revenue.

Luxury watch sales peaked in 2021, and demand for brands other than Rolex and Patek Philippe slowed. We initiated a position in early 2024 after the resulting decline in the share price.

Unfortunately, WOSG faced another setback when the United States imposed 39% tariffs on Swiss imports. We feared the economics of the business could deteriorate sharply. Rolex boutiques are difficult to repurpose, and passing through a 39% price increase, even in the luxury segment, seemed like a tall order.

We were patient. Switzerland was unlikely to be singled out as the root-cause of the US trade imbalance forever. And in a worst case, the tariffs would likely accelerate the consolidation in the industry, benefiting the strongest players.

With tariffs now finally in the rear-view mirror, WOSG is finally back to executing its proven playbook. US growth re-accelerated to 24%. The UK is steady at 5% growth. The balance sheet is underleveraged. Despite the strong move-up, shares are trading at 13x next year’s earnings. WOSG remains a conviction long.

Conclusion

The market has become a one-trick pony with many quality companies being sold off in favor of anything that touches the AI trade. We are happy to buy quality companies at depressed valuations. Meanwhile we are doing our own thing, allocating to sectors with structural tailwinds that are largely overlooked, including the aerospace aftermarket, futures commission merchants, and various payment companies.

By following this disciplined strategy, we have been compounding capital at well over 20% since inception while providing good diversification to anyone who is invested in the major indices. This has also resulted in very low volatility, and we have not seen any major drawdowns in our portfolio to date.

On behalf of the Night Watch team,

Roderick van Zuylen, Chief Investment Officer

Eileen Ke, Chief Operating Officer

Night Watch Investment Partners LP – Net Performance (in USD)

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.